Oil has been the central nervous system of the global economy for over a century. Bitcoin has existed for barely more than a decade. Yet, during periods of geopolitical stress and commodity volatility, market participants increasingly ask whether oil shocks and Bitcoin move together — and if so, why.

This analysis examines historical episodes of energy disruption and evaluates how Bitcoin price action, liquidity cycles, and macro regime shifts interact with oil-driven volatility.

What Is an Oil Shock?

An oil shock is a rapid and substantial increase in crude oil prices, typically triggered by:

- Geopolitical conflict

- Supply disruption

- Production cuts

- Sanctions

- Transportation chokepoints

Historically, oil shocks have transmitted through the economy via three primary channels:

- Inflation pressure

- Growth slowdown

- Financial tightening

Oil is embedded in transportation, agriculture, manufacturing, and consumer goods. When energy costs spike, input costs rise system-wide. This compresses margins and reduces discretionary spending.

Before Bitcoin existed, oil shocks were primarily studied through their effects on equities, bonds, gold, and currency markets. Now, we must include digital assets in the analysis.

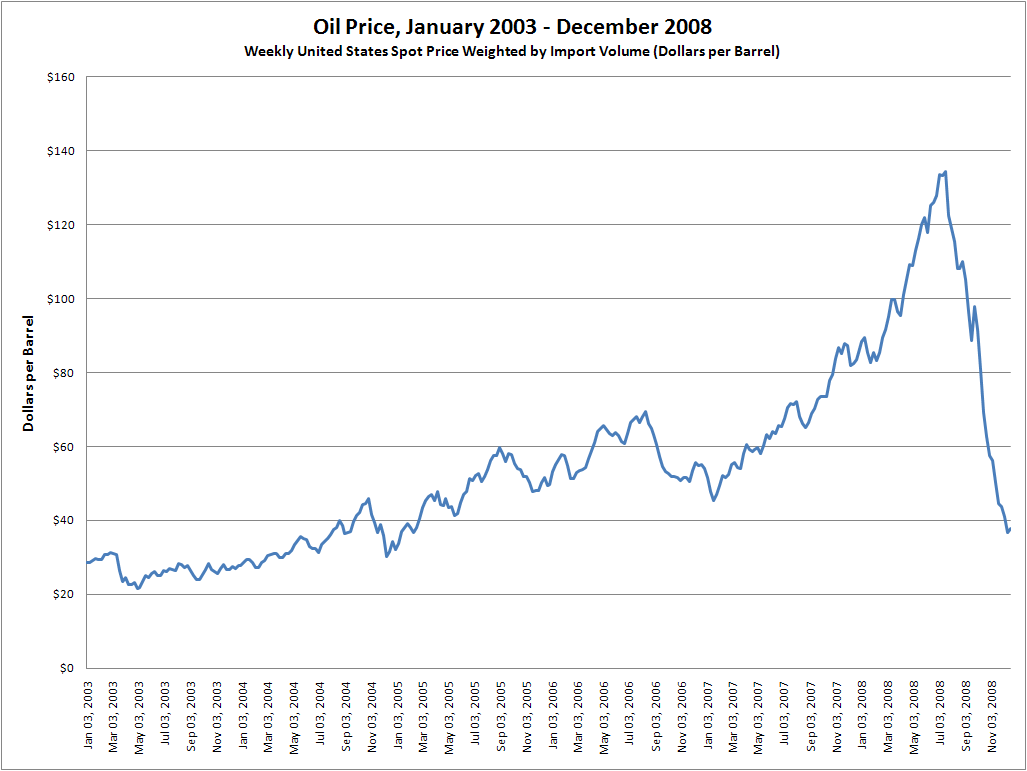

The 2008 Oil Spike and the Birth of Bitcoin

In 2008, oil reached approximately $147 per barrel before collapsing during the global financial crisis.

At that moment:

- Inflation surged

- Growth expectations deteriorated

- The financial system seized

- Central banks launched massive liquidity programs

Shortly afterward, the Bitcoin whitepaper was released by Satoshi Nakamoto.

While Bitcoin was not yet trading during the oil spike, its ideological foundation was born in an environment of:

- Monetary expansion

- Bank bailouts

- Sovereign debt growth

- Distrust in financial intermediaries

This context matters. Bitcoin’s design is explicitly anti-inflationary — fixed supply, predictable issuance, and no central authority.

However, from a market correlation standpoint, we cannot yet analyze price behavior. That begins in 2011.

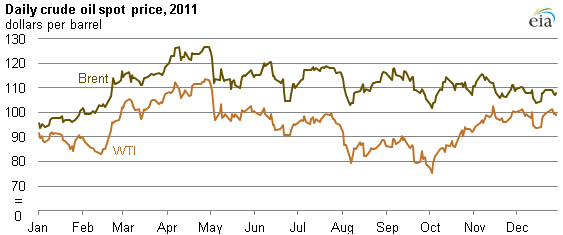

2011–2014: Arab Spring and Early Bitcoin Cycles

The Arab Spring created instability across North Africa and the Middle East, contributing to elevated oil prices from 2011 to 2013.

Bitcoin during this period:

- Experienced its first major bull run (2011)

- Crashed

- Then surged again into 2013

Correlation between oil and Bitcoin during this phase was weak.

Why?

Because Bitcoin was still:

- Illiquid

- Retail-driven

- Structurally immature

- Detached from institutional macro flows

Oil prices were elevated, but Bitcoin’s moves were primarily driven by:

- Exchange adoption

- Early speculative cycles

- Technical network growth

Conclusion for this era: No reliable correlation.

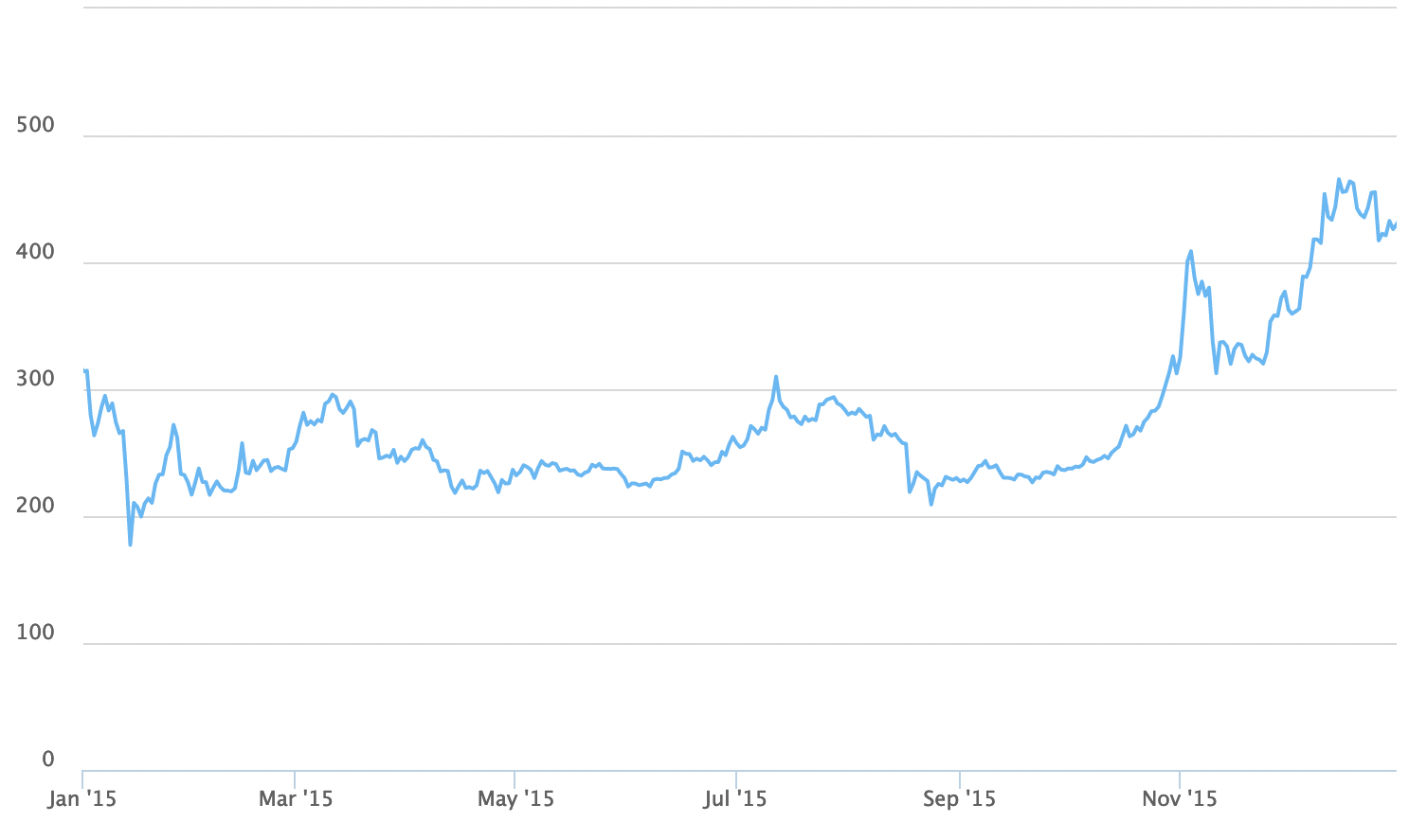

2014–2016: Oil Collapse and Bitcoin Consolidation

In late 2014, oil collapsed from above $100 to below $40 due to:

- OPEC supply decisions

- U.S. shale expansion

- Global demand slowdown

Bitcoin during this period:

- Fell from its 2013 highs

- Entered a prolonged bear market

- Consolidated through 2015

Did oil cause Bitcoin weakness?

Unlikely.

Instead, Bitcoin’s downturn was largely driven by:

- The Mt. Gox collapse

- Exchange failures

- Early market immaturity

However, one structural pattern emerges:

Oil collapse reduced inflation pressure globally.

Central banks stayed accommodative.

Liquidity remained abundant.

Bitcoin bottomed and began recovery into 2016–2017.

Indirectly, the liquidity environment mattered more than oil prices themselves.

2020: Pandemic Oil Crash and Liquidity Explosion

April 2020 marked a historic anomaly: oil futures briefly traded negative.

Simultaneously:

- Global growth collapsed

- Markets crashed

- Central banks unleashed unprecedented stimulus

The Federal Reserve expanded its balance sheet dramatically.

Bitcoin initially fell during the March liquidity crisis.

Then it rallied aggressively into 2021.

Key takeaway:

It wasn’t oil that drove Bitcoin.

It was liquidity expansion, money supply growth, and falling real yields.

Oil’s collapse was a symptom of demand destruction. The response to that collapse — monetary stimulus — fueled the crypto bull market.

2022: Russia-Ukraine War and Energy Inflation

The conflict between Russia and Ukraine triggered one of the largest energy supply disruptions in decades.

Oil spiked above $120.

Natural gas prices surged in Europe.

Inflation accelerated globally.

Central banks responded by tightening aggressively.

Bitcoin fell sharply throughout 2022.

At first glance, this appears to show:

Oil spike → Bitcoin decline.

But again, the mechanism was indirect.

Oil contributed to inflation.

Inflation forced central banks to raise rates.

Higher rates increased real yields.

Rising real yields reduced liquidity.

Liquidity contraction pressured risk assets, including crypto.

Thus, oil shock correlated negatively with Bitcoin during this cycle — but via monetary tightening.

Structural Framework: How Oil Affects Bitcoin Indirectly

To formalize the relationship:

Oil Shock → Inflation Pressure → Central Bank Response → Liquidity Regime → Bitcoin

Bitcoin does not respond to oil directly.

It responds to:

- Liquidity conditions

- Real interest rates

- Dollar strength

- Risk appetite

We can classify outcomes:

- Oil spike + accommodative policy → Potentially bullish

- Oil spike + tightening policy → Bearish

- Oil collapse + stimulus → Bullish

- Oil collapse + recession + no stimulus → Neutral to bearish

Bitcoin trades as a liquidity-sensitive macro asset, not as an energy derivative.

Is Bitcoin a Hedge Against Oil Inflation?

This remains debated.

Gold has historically acted as a partial hedge during commodity-driven inflation.

Bitcoin’s behavior is more nuanced.

During inflation driven by:

- Supply shocks

- Energy disruption

- Tight monetary response

Bitcoin has struggled.

During inflation driven by:

- Excess monetary expansion

- Currency debasement fears

Bitcoin has outperformed.

Thus, Bitcoin is more sensitive to monetary inflation than commodity inflation.

The Dollar Variable

Oil is priced globally in U.S. dollars.

When oil spikes:

- The dollar may strengthen due to safe-haven demand

- Or weaken if deficits expand

Bitcoin is highly inversely correlated to the dollar index in many cycles.

Strong dollar regimes have historically suppressed crypto performance.

Therefore, oil shocks that strengthen the dollar can pressure Bitcoin.

Long-Term Perspective

Over a multi-year horizon, repeated oil shocks contribute to:

- Persistent fiscal deficits

- Defense spending

- Structural inflation risk

- Sovereign debt accumulation

If governments respond with monetization or financial repression, Bitcoin’s scarcity narrative strengthens.

However, this plays out over years, not weeks.

Short-term correlation is dominated by liquidity.

Long-term correlation is dominated by monetary credibility.

Conclusion: Correlation Is Regime-Dependent

The historical record shows:

There is no stable, direct correlation between oil prices and Bitcoin.

Instead, the relationship is conditional:

- Oil affects inflation.

- Inflation influences central bank policy.

- Policy determines liquidity.

- Liquidity drives Bitcoin.

If evaluating future geopolitical risk in the Middle East or elsewhere, the key question is not:

“Will oil rise?”

The critical question is:

“How will central banks respond?”

Bitcoin is ultimately a function of monetary regime, not crude supply.

Understanding that transmission mechanism is the difference between narrative-driven speculation and macro-informed positioning.