What Is Private Credit?

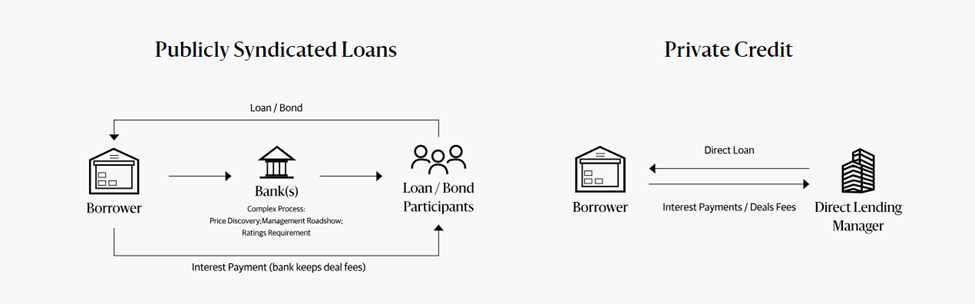

At its core, private credit refers to loans made by non-bank institutions directly to companies. Instead of borrowing from traditional banks, businesses increasingly turn to private funds, asset managers, or institutional investors for capital.

This form of financing—often called direct lending—has become one of the most important shifts in modern finance. These loans are typically negotiated privately, meaning they are not traded on public markets and are often tailored to the borrower’s specific needs.

In practice, the structure is simple:

- Investors allocate capital to a private credit fund

- The fund lends directly to companies

- Borrowers repay with interest (often higher than bank loans)

The appeal is clear: investors gain access to higher yields, while companies gain access to flexible capital that banks may no longer provide.

Why Private Credit Is Booming

The growth of private credit has been nothing short of explosive. The market is estimated to reach $1.67 trillion in 2025 and could approach nearly $3 trillion by 2030, driven by strong investor demand.

Several structural forces are driving this expansion:

1. Bank Retrenchment

After the global financial crisis, banks faced stricter regulations and capital requirements. This made certain types of lending—especially to mid-sized companies—less attractive. Private credit stepped in to fill that gap.

2. The Search for Yield

In a world where traditional fixed income often delivers modest returns, investors are increasingly drawn to higher-yielding private loans.

3. Institutional Demand

Pension funds, insurers, and sovereign wealth funds have significantly increased allocations to private markets. Large firms like Apollo Global Management, Blackstone, and Ares Management dominate this space.

4. Expansion Beyond the Middle Market

Private credit initially focused on mid-sized companies but now finances multi-billion-dollar deals, competing directly with traditional banks.

How Private Credit Actually Works

Understanding the mechanics of private credit is key to grasping its importance.

The Lending Process

- A company seeks financing (often for growth, acquisitions, or refinancing)

- A private credit fund evaluates the borrower’s financial health

- The fund structures a customized loan (interest rate, covenants, maturity)

- The loan is held privately—not traded on public markets

Unlike banks, private lenders can move quickly and tailor deals, often accepting more complexity in exchange for higher returns.

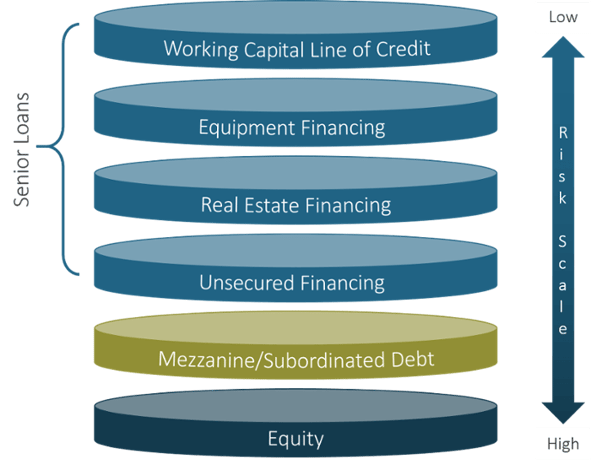

Common Types of Private Credit

- Direct Lending – Loans directly to companies

- Unitranche Loans – Blended senior + subordinated debt

- Mezzanine Financing – Hybrid of debt and equity

- Asset-Based Lending – Loans backed by collateral

These structures allow lenders to optimize risk and return across different scenarios.

The Biggest Private Credit Lenders

The private credit ecosystem is dominated by a handful of massive asset managers. These firms control hundreds of billions in capital and increasingly rival traditional banks.

Key Players

- Apollo Global Management

- Blackstone

- Ares Management

- KKR

- The Carlyle Group

- Oaktree Capital Management

- Goldman Sachs Asset Management

These firms are not just participants—they are shaping the entire market. In fact, the largest managers collectively control trillions in credit assets, reflecting how concentrated and institutionalized the space has become.

Notably, Apollo Global Management alone has been identified as one of the largest private credit managers globally, with hundreds of billions deployed.

Why Investors Love Private Credit

The appeal of private credit lies in its unique investment profile.

1. Higher Yields

Private loans typically offer higher interest rates than public bonds, compensating investors for illiquidity and risk.

2. Floating Rates

Many loans are structured with floating interest rates, which perform well in rising rate environments.

3. Downside Protection

Loans are often secured and sit higher in the capital structure, meaning lenders get paid before equity holders.

4. Portfolio Diversification

Private credit has low correlation with public markets, making it attractive for diversification.

The Hidden Risks in Private Credit

Despite its advantages, private credit is not without risk—and these risks are increasingly coming into focus.

1. Illiquidity

Investors cannot easily exit positions. Unlike stocks or bonds, these loans are not actively traded.

2. Opacity

Private markets lack transparency, making it harder to assess true risk levels.

3. Credit Risk

Borrowers are often smaller or more leveraged companies, increasing the chance of default.

4. Liquidity Stress

Recent developments show that some funds have begun limiting withdrawals amid rising investor concerns.

5. Systemic Concerns

There are growing fears that private credit could introduce broader financial risks, especially as the market scales and becomes more interconnected.

Private Credit vs Traditional Bank Lending

| Feature | Private Credit | Traditional Banks |

|---|---|---|

| Speed | Fast | Slower |

| Flexibility | High | Limited |

| Regulation | Lower | High |

| Interest Rates | Higher | Lower |

| Liquidity | Low | Higher |

Private credit’s competitive advantage lies in its ability to move quickly and customize deals, but that flexibility comes at a cost—higher risk and less oversight.

The Future of Private Credit

The future of private credit is both promising and uncertain.

On one hand, the market continues to expand rapidly, with projections suggesting trillions more in assets under management over the coming decade.

On the other hand, recent market stress—ranging from redemption limits to valuation concerns—suggests the asset class may be entering a more volatile phase.

Key trends to watch:

- Increased retail investor access

- Growth in asset-backed and infrastructure lending

- Greater regulatory scrutiny

- Integration with insurance and pension capital

Final Thoughts

Private credit has fundamentally reshaped the global lending landscape. What began as a niche alternative to bank loans has evolved into a multi-trillion-dollar industry dominated by some of the largest financial institutions in the world.

Its appeal—yield, flexibility, and diversification—is undeniable. But so are its risks: illiquidity, opacity, and potential systemic exposure.

For investors and observers alike, the key question is no longer whether private credit matters—it clearly does.

The real question is:

Will private credit prove to be one of the most important innovations in modern finance…

or the next major stress point in the financial system?