For years, the crypto conversation has centered around one big idea: Bitcoin replacing traditional money. While that narrative captures headlines, something quieter — and potentially more transformative — is happening underneath the surface of the financial system.

The rise of stablecoins is reshaping how money moves across the world. These digital assets, pegged to traditional currencies like the US dollar, are rapidly becoming the infrastructure layer of modern finance. In many ways, they are doing what early cryptocurrency advocates hoped blockchain would accomplish: enabling fast, borderless, programmable money.

But the most surprising part of the story is this: stablecoins may replace key functions of banks long before Bitcoin replaces fiat currency.

The Rise of Stablecoins: Digital Dollars on the Blockchain

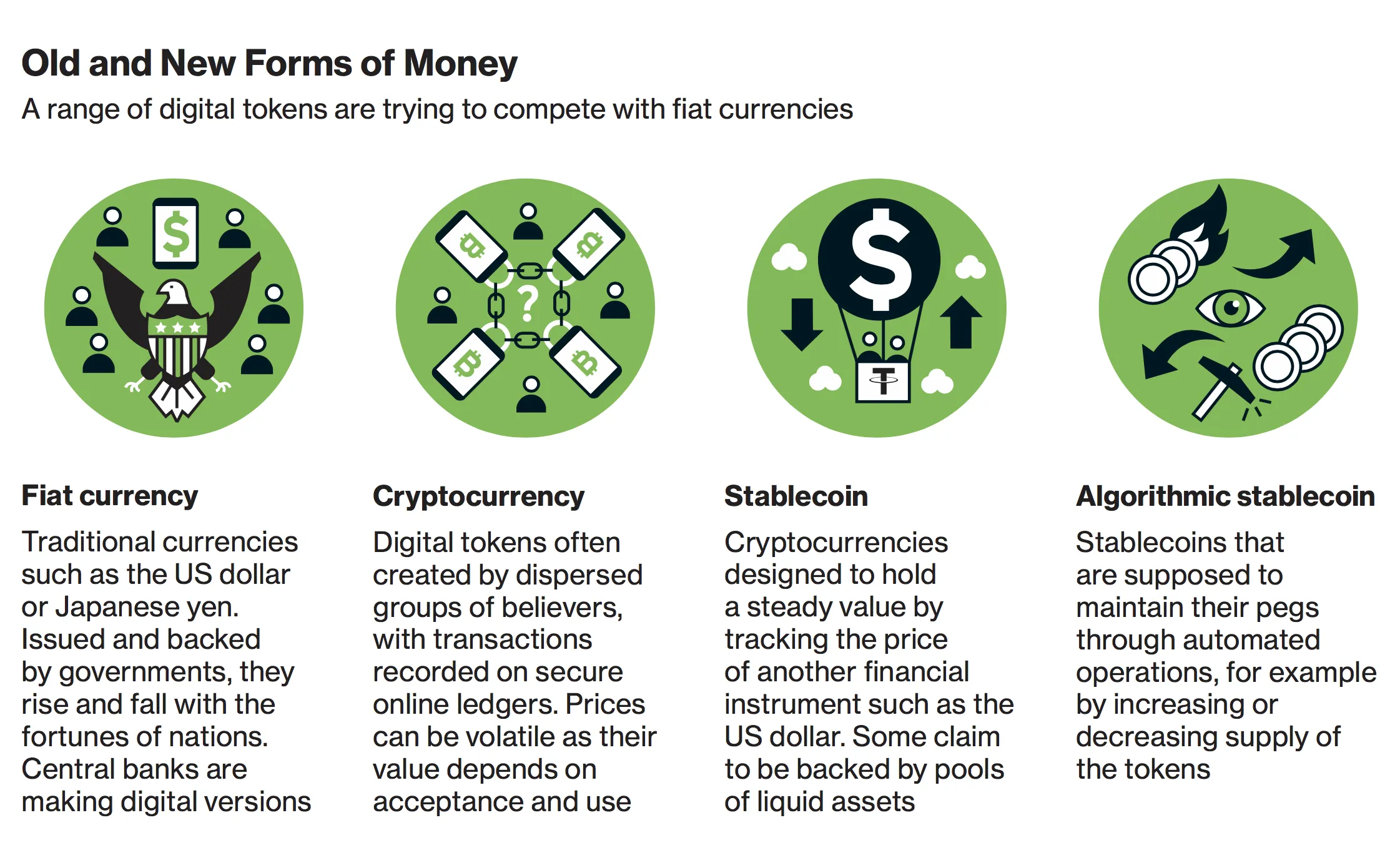

At their core, stablecoins are cryptocurrencies designed to maintain a stable value, typically pegged to a fiat currency like the US dollar. The most widely used examples include USDT (Tether) and USDC (USD Coin), which are backed by reserves intended to maintain their one-to-one relationship with the dollar.

Unlike highly volatile cryptocurrencies, stablecoins provide price stability while still benefiting from the advantages of blockchain technology. Transactions settle within minutes, fees are typically far lower than traditional banking transfers, and the system operates globally without relying on legacy financial rails.

This combination has made stablecoins one of the fastest-growing sectors in crypto. Today, hundreds of billions of dollars move through these digital assets every month. They are used for trading, payments, lending, remittances, and decentralized finance.

In effect, stablecoins are becoming digital dollars that operate outside the traditional banking system.

Why Stablecoins Are Growing Faster Than Traditional Banking Rails

One of the biggest reasons stablecoins are gaining traction is efficiency. Traditional banking infrastructure was built decades ago and relies on layers of intermediaries. A typical international transfer may pass through multiple banks, clearing systems, and compliance checks before reaching its destination.

This process can take days and often involves significant fees.

By contrast, stablecoin transactions settle almost instantly on blockchain networks. Instead of relying on multiple intermediaries, transfers are validated by decentralized networks such as Ethereum, Solana, or Tron.

For businesses and individuals moving money across borders, the difference is dramatic:

- Bank wires may take 1–3 business days

- Stablecoin transfers often settle within minutes

For emerging markets in particular, this technology is transformative. Millions of people in countries with unstable banking systems are already using stablecoins as a digital savings account denominated in dollars.

This phenomenon has effectively created a parallel global financial system — one that operates 24/7 and requires nothing more than a smartphone and internet connection.

Stablecoins and the Quiet Transformation of Finance

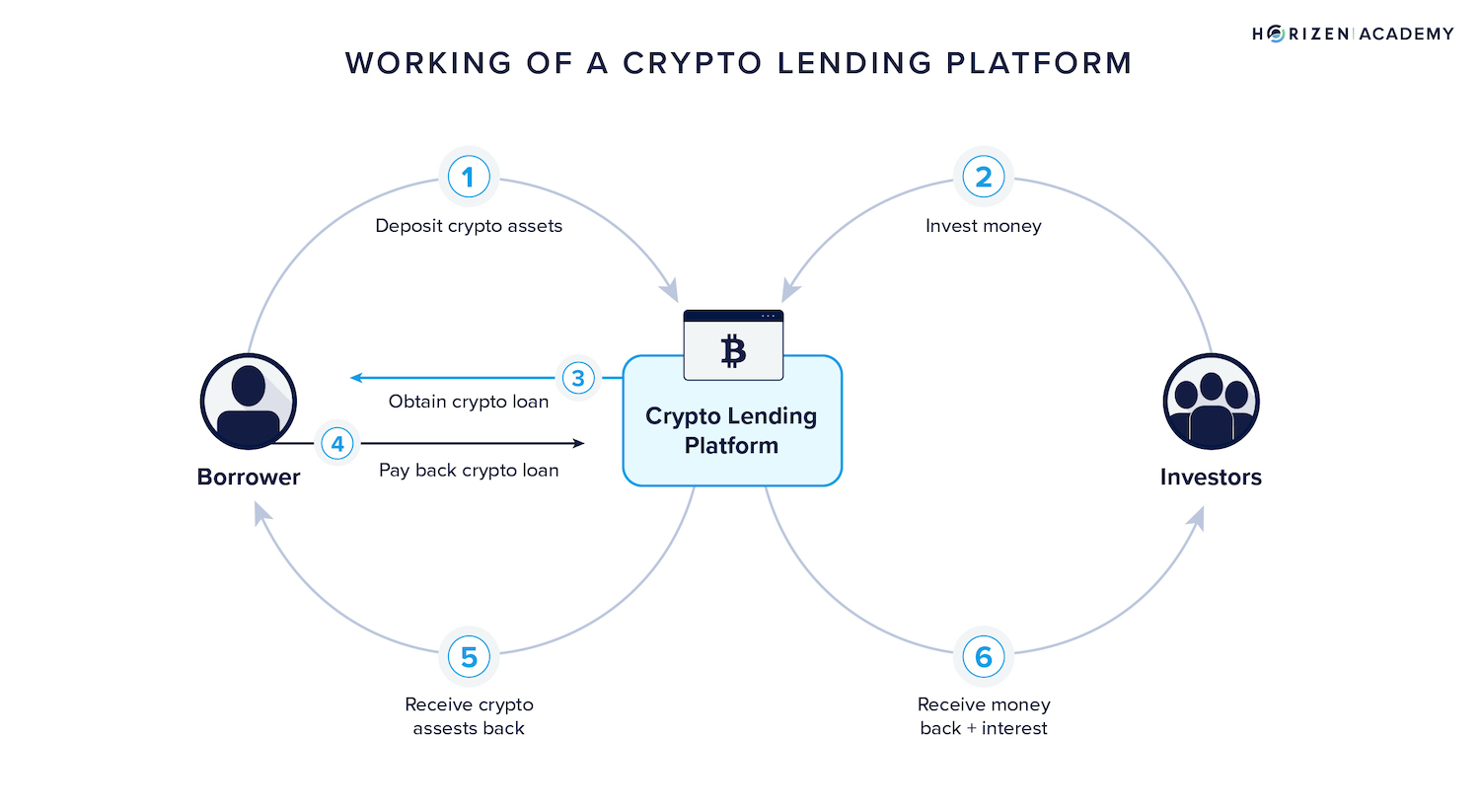

Beyond payments, stablecoins are also powering the rapid growth of decentralized finance (DeFi). In traditional finance, banks provide services like lending, borrowing, interest-bearing accounts, and liquidity provision.

But blockchain protocols now offer many of the same services — often using stablecoins as the base currency.

Users can:

- Lend stablecoins and earn yield

- Borrow against crypto collateral

- Provide liquidity in decentralized exchanges

- Participate in automated financial markets

These services operate through smart contracts rather than centralized institutions. Instead of trusting a bank to manage accounts and loans, users interact with transparent code on public blockchains.

While the technology is still evolving, the implications are enormous. If stablecoins become the primary settlement asset of decentralized finance, then much of the banking infrastructure could eventually be replicated by software.

This doesn’t necessarily mean banks will disappear, but their role may fundamentally change.

Why Governments and Banks Are Paying Attention

The rapid adoption of stablecoins has not gone unnoticed by governments and financial institutions.

Regulators increasingly view them as systemically important financial infrastructure. After all, if billions of dollars move through stablecoins daily, they effectively function as digital versions of traditional currency.

This has sparked a wave of regulatory discussions around the world.

Some policymakers are exploring frameworks that would allow stablecoin issuers to operate similarly to regulated financial institutions. Others are considering the introduction of central bank digital currencies (CBDCs) as a government-controlled alternative.

At the same time, many banks are exploring partnerships with blockchain companies or experimenting with issuing their own tokenized deposits.

The growing interest from regulators and banks signals something important: stablecoins are no longer a fringe crypto experiment. They are rapidly becoming a central component of global financial innovation.

Stablecoins as the Foundation of the Digital Economy

As the digital economy continues to expand, the need for internet-native money becomes increasingly clear. Online marketplaces, global freelancers, gaming ecosystems, and digital creators all require payment systems that are fast, programmable, and borderless.

Stablecoins are uniquely positioned to fill that role.

Unlike traditional bank transfers, blockchain-based payments can integrate directly into software platforms. Smart contracts allow money to move automatically when conditions are met, enabling entirely new financial applications.

For example:

- Freelancers can receive instant cross-border payments

- Online businesses can automate payouts globally

- Digital platforms can distribute revenue in real time

- Developers can build programmable financial systems

In this environment, stablecoins function less like speculative crypto assets and more like digital infrastructure.

They become the monetary layer of the internet.

Why Bitcoin and Stablecoins Serve Different Roles

The rise of stablecoins doesn’t diminish the importance of Bitcoin. Instead, it highlights how different types of cryptocurrencies may serve different roles within the financial ecosystem.

Bitcoin is often described as digital gold — a scarce asset designed for long-term value preservation. Its volatility and limited supply make it attractive as a store of value, but less ideal for everyday transactions.

Stablecoins, on the other hand, function as digital cash.

They provide the stability necessary for commerce, lending, and financial services while maintaining the speed and accessibility of blockchain networks.

Together, these two categories may form the backbone of the crypto economy:

- Bitcoin as a global store of value

- Stablecoins as the transactional layer of finance

In that sense, the evolution of crypto mirrors traditional markets, where gold and dollars serve distinct purposes.

The Future: A Financial System Built on Blockchain

The next decade may witness a dramatic shift in how money moves around the world. As blockchain technology matures and regulatory clarity improves, stablecoins could become the default settlement layer for digital finance.

This doesn’t necessarily mean banks will vanish. Instead, financial institutions may evolve into custodians, compliance providers, and infrastructure operators within blockchain networks.

But the underlying rails of the financial system may look very different from today.

Rather than relying on slow clearing networks and intermediary banks, transactions could move across decentralized networks using stablecoins as the primary medium of exchange.

If that future unfolds, one thing becomes clear:

stablecoins may transform finance long before Bitcoin replaces traditional money.

And by the time the broader public realizes what has happened, the global financial system may already be running on blockchain rails.